March 16, 2026, By Chet Haskell – Private college and university endowments have been much in the news of late. Most of the attention has been paid to the small group of private non-profit universities with endowments in excess of $10 billion. Federal legislation has increased the tax on these very large endowments. The Trump Administration has sought – and in some cases succeeded – to get payments to “settle” claims against the university and to restore suspended Federal research funding. But focusing on these institutions obscures some important perspectives on endowments and, by extension, their use.

What are the data?

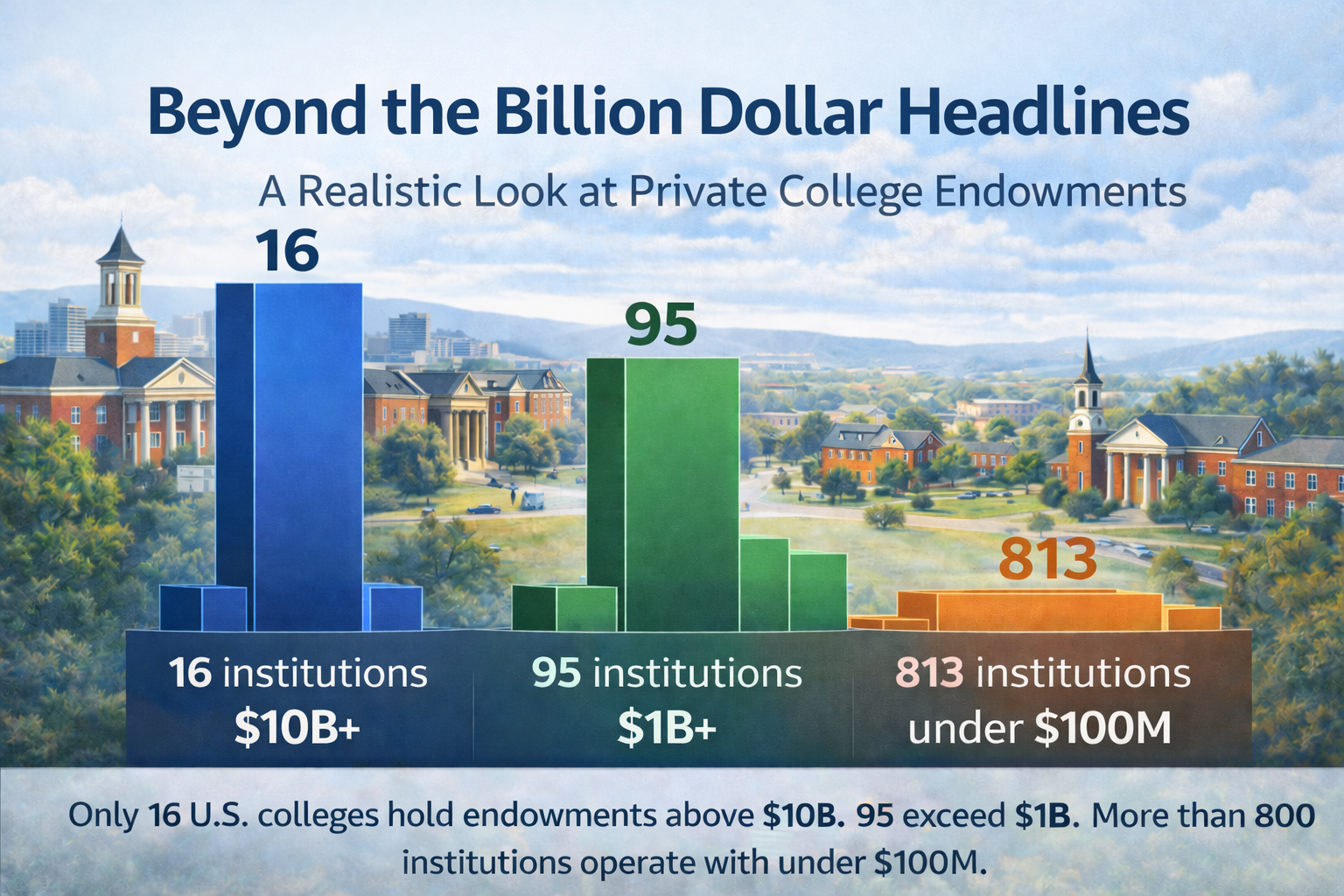

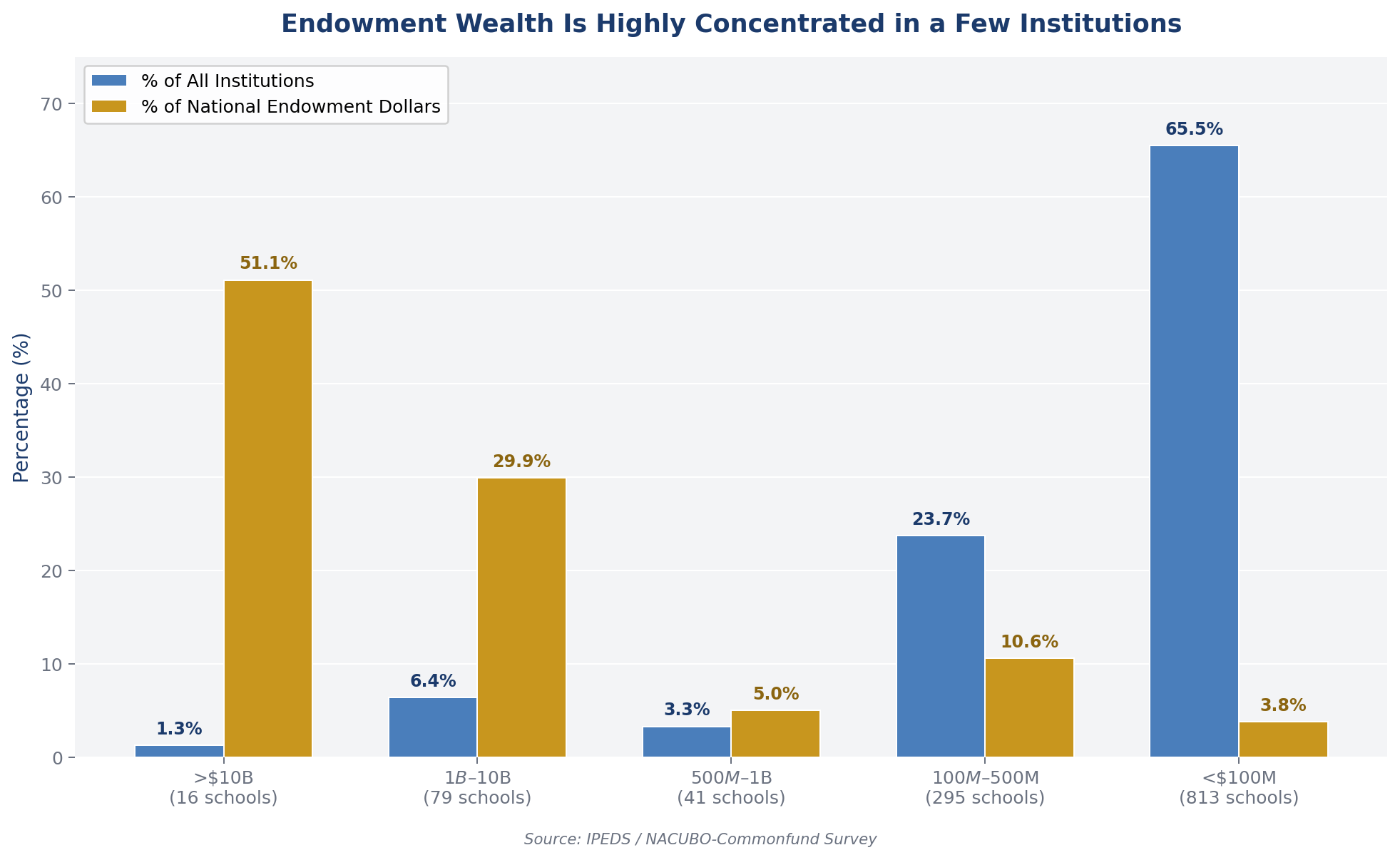

First, the data demonstrate that the vast majority of endowment assets in American higher education are held by a small percentage of wealthy institutions. According to IPEDS data corroborated by the annual NACUBO Commonfund survey, there are only 16 institutions with endowments in excess of $10 billion. These represent a tiny fraction (1.3 percent) of the 1243 private institutions with endowments (and another 328 without endowments). Yet, together they represent more than 50% of all endowments in terms of dollar value ($326.4 billion of a national total of $638.1 billion).

There are another 79 institutions with reported endowments in excess of $1 billion, representing 6.4% of the institutions and 29.9 percent of the national total. There are also 41 institutions with endowments between $500 million and $1 billion. Thus, together, these 136 institutions control total endowment assets in excess of $548 billion. Put differently, these institutions represent 10.9% of all private institutions with endowments, but also control 85.9% of all private endowment dollars.

At the next level, there are 295 institutions with more than $100 million and less than $500 million in endowments. These average $220 million and represent 10.6% of the national total.

Together, the 430 institutions with endowments in excess of $100 million represent 34.6 percent of all private institutions and a staggering 96.2% of total national endowments.

At the lowest level, the 813 institutions with small endowments (less than $100 million, averaging $30 million) are in essence holding almost nothing. They represent 65% of all private colleges, but hold only 3.8% of national endowment assets. This situation is dire for many reasons. These 813 institutions are financially insecure and may lack the resources or the scale to improve their positions independently. They are most at risk to join the growing list of institutional closures. Many of these institutions are venerable anchors of small communities and have played an important role in the diverse ecosystem of American higher education. They have a wide range of missions, specializations, and academic offerings. Yet, they almost uniformly lack the financial basics for longer-term security.

As will be argued below, the 295 institutions with endowments in excess of $100 million (average endowments of $220 million) are also at risk, given the changing demographics and economics of the higher education landscape. While these institutions are unlikely to collapse completely, they are under significant pressure to change their strategies and to consider the impacts of what many observers have dubbed a “coming era of consolidation.”

A final note about very small institutions. IPEDS also identifies 328 institutions without any endowment. Most are tiny specialized or religious colleges, and others have already announced pending closure.

There are also large endowments among some of the public institutions or systems. NACUBO identifies the following examples. There are eight public entities with endowments in excess of $5 billion for a total of $138.7 billion and an average of $17.3 billion. (These data are skewed by the University of Texas Systems $48 billion endowment, much of which comes from State oil revenues.)

The principal difference between these endowments and those of the private institutions is not size, but another measurement: endowment per student. The eight top public institutions have an average per student endowment of $267 thousand, while the eight top private institutions have per student endowments averaging $1.94 million. This perspective will be discussed further below.

What are the limitations of endowments?

First, we must be clear about what endowments are and are not. Endowments, whatever the size, are not simply a pot of money an institution can dip into as needed. Instead, almost all endowments are restricted in various ways as to their use. According to NACUBO, approximately 48% of endowments are restricted to student financial aid purposes. This is of obvious importance, as such aid not only attracts students and facilitates enrollments, but also represents real cash going into an institution’s operating budget. Such aid is of particular importance at a time when most private institutions are discounting their tuition by 50% or more.

There are many other forms of restriction. Buildings, faculty positions, specific programs, and even football coaches are often funded from restricted endowments. Again, these specific purposes limit an institution’s flexibility, especially in times of financial crisis. In effect, a college or university endowment is a pool of separate endowments, each with its own restrictions and purposes. However, neither these funds nor their generated incomes are typically fungible for budgetary purposes.

There are examples of institutional donor-funded endowments that are not restricted to particular uses. These represent a small minority of endowed funds, as most donors have a particular purpose for their gift. Finally, as discussed below, there is a category of quasi-endowments where the institution has decided to fence in certain assets as a form of reserve fund controlled by an institution’s board.

The fundamental concept behind endowments is support of an institution’s mission and existence over long time periods (and the “perpetuity nature” of most endowments is designed as support over VERY long times). While providing funding for the future is an important aspect of institutional sustainability, restricting funding purposes may be counterproductive. Specific purposes – or indeed, institutions themselves – may have no relevance today or in the future. Should institutions exist forever? Should they always maintain the same purposes? Should the restricted purposes continue forever?

Institutions seeking to modify or repurpose a restricted endowment face significant challenges. The guiding principle is the intent of the original donors in making the endowment gift. With donor concurrence, a change in restrictions is simple. However, the donors of many endowments may wish to permit such changes or may not even be alive to consider doing so. In such cases, an institution must get the approvals of probate courts and, in some cases, state Attorneys General, a time-consuming and difficult process.

How do endowments affect budgets?

The traditional rule of thumb for most institutions is to limit the actual use of endowments to a portion of the income generated annually. A common metric is 5% of the value of the endowment. In other words, an endowment of $50 million will be expected to generate roughly 5% or less ($2.5 million) for annual expenditure purposes. Even this is limited, as most institutions try to reinvest income into capital in order to maintain value. If, as in recent years, an endowment actually generates more than 5%, the institution may choose to utilize or recapitalize the excess.

While the wealthy institutions have more capacity to exceed 5% returns and thus decide strategies, 5% is the general rule for smaller institutions. However, as Robert Kelchen points out in a recent blog, more and more schools have increased the draw on their endowments. Of 1202 institutions he studies, in 2024, 43% spent between 4% and 6%. In other words, they spent within the range of the general metric. At the same time, 8% of institutions spent more than 10%. And 13% spent zero, as most of these were tiny institutions with less than $5 million in endowment. (Kelchen citation)

And the $2.5 million in this illustrative example represents multiple purposes and is of limited fungibility. Most likely, half is dedicated to student financial aid. Again, this is important because it represents “real” money, as opposed to discounted aid. Endowment funded student aid contributes dollar for dollar to institutional net tuition revenue, whereas discounted aid means a reduction in net tuition revenue. And for all smaller institutions, net tuition revenues (an effective measure of the value of enrollments) is the coin of the realm.

But using $1.25 million for aid means there is only a similar amount available for all other budget purposes. In a typical operating budget of $80 million, this represents less than 2% of needed revenue. Helpful, but not decisive in financial terms.

Another key concept for endowments (and gifts in general) is whether or not they are substitutional – they pay for a necessary expense (like faculty), thus freeing up tuition dollars for other purposes. A properly funded faculty chair for an essential faculty member “relieves” the general budget from having to fund it. And tuition dollars, once received, can be used for any purpose the institution deems proper.

Unfortunately, many institutions have accepted restricted gifts that are incremental in budget terms – they add to the expense budget. The classic example is the endowment gift for a new facility that does not cover the true cost of ongoing facility maintenance. Or an endowment creates a new program that simply is not fully funded, thus requiring subsidization from other budget resources.

In short, in almost every case, endowments are not the answer to institutional funding challenges. Yes, they can contribute to the bottom line, but it takes a very large endowment to relieve institutions of the need for enrollments and tuition revenue. Indeed, endowments can be a kind of buffer against reality when institutions feel secure in their endowment and fail to take forward-looking strategic decisions.

Even the very largest endowments do not always protect the institutions. During the dramatic stock market declines in 2008-2009, some of the wealthiest institutions cut expenses, laying off employees and shuttering programs. Why? If endowment income covers 20% of the $2 billion operating budget of an institution and that income falls by half, that institution suddenly has a $200 million hole in its annual budget.

There is a category of institutional surpluses often called “quasi-endowments.” An institution fortunate to have a cash surplus may decide to set it aside from regular considerations by imposing board of trustee restrictions on its use. This prudent measure enables an institution to protect such a fund while reserving the capacity for the board to lift restrictions if it so wishes.

The absence of such cash reserves is an Achilles heel for many smaller institutions. If annual financial success is defined as a balanced operating budget, the institution will face difficulty if harder times come unexpectedly or if an opportunity for growth through investment arises. Every institution should do all it can to create cash reserves, even if very modest in scale. Doing so is an indicator of fiscal probity that may provide some room for maneuver either to deal with a crisis or to fund an investment.

What are the strategic considerations?

A rhetorical question that should face every president and CFO is: Would you rather have endowment gifts or current use gifts? Would you rather have a $10 million endowment gift that will generate $500,000 every year in perpetuity or would you rather have three annual current use gifts of $3.3 million? If your short-term future is under stress, the endowment income may be of limited utility, whereas the larger current use income may enable you to make investments or changes necessary to ensure enrollment growth and sustainability.

The strategic plans of most smaller institutions often call for establishing endowed funds of a certain scale. This may not be the best strategy. In the first instance, endowment gifts usually require long periods of engagement and cultivation with potential donors, and time is not on the side of institutions under pressure. While most institutions are unlikely to decline a sizeable endowment gift unless it is truly incremental or it would skew the basic mission, institutions based on enrollments (namely, almost all) must be able to have funding to invest in initiatives designed to grow those enrollments in the near term. An announced strategic goal of establishing an endowment of $100 million may be laudable. But even if achieved, it may not be sufficient to help short-term budgets.

There are examples of smaller institutions engaging in significant capital campaigns that involve a mixture of longer-term endowment objectives. These include restricted endowments for purposes like scholarships or faculty positions and unrestricted funds, as well as amounts of current use non-endowed funds. This type of approach can be successful if there is a strong alumni donor base and there are opportunities for very large gifts. But as all academic development staff know, preparation for such a campaign takes tremendous seedwork and preparation. This approach is unlikely to be successful with institutions lacking a long-term donor engagement and cultivation record.

Another more subjective possibility is the degree to which a commitment to such a campaign strengthens the institution. Perhaps large gifts stimulate other large gifts. Perhaps the raised profile of an institution and its avowed direction encourages potential students choose to enroll. A basic purpose of such a campaign is to make an institution more attractive to students, including through such objectives as new facilities, increased scholarship aid or new programs. It is difficult to imagine a capital campaign that does not also seek to encourage enrollment growth.

The reality – as is often said – is that the three most important things for private higher education are enrollments, enrollments, and enrollments. Sustaining and building enrollments is a complex, Herculean task in an extremely competitive environment. Focusing on enrollment growth – and specifically, net tuition revenue growth – must be the highest priority. The more than 800 institutions with endowments smaller than $100 million are not going to be saved by anything except enrollment growth. Gifts and endowments are positive, but rarely make the survivability difference for smaller institutions.

Conclusion

Indeed, in the context of the current undergraduate demographic decline and the rising costs of providing competitive higher education program, it is hard not to conclude that many smaller institutions will either find some form of partnership or merger in order to achieve economies of scale and resources or they will fail.

The 295 institutions with endowments between $100 million and $500 million are best placed to control their destinies, not because their endowments alone will sustain them, but because they have sufficient resources to buy some time and implement new strategies. Their resources will likely provide opportunities for them to initiate partnerships or to absorb other, weaker partners. But it is incumbent upon their leadership to be clear-eyed about their strategies and the implementation of these plans.

The 813 institutions with endowments less than $100 million have much less room to maneuver. One possibility is to seek a partnership where they are acquired or are the junior partner. Another is to try to band together with like institutions to build scale. However, it will become increasingly difficult for these institutions to “go it alone.” In the absence of significant enrollment growth, they will always be at high risk.

There is an important potential role for philanthropy here. One example is the Transformational Partnerships Fund, the supporters of which include the Kresge Foundation. This Fund seeks to encourage partnerships between institutions by providing grants for technical, legal, and consulting resources, although their maximum grant of $100,000 is clearly insufficient, especially for institutions already in significant financial trouble. Another example is the State of New Jersey program to encourage consolidation of institutions in that State. The fact of the matter is that it is expensive and time-consuming to plan and consummate a partnership agreement in any circumstance. The institutions most in need of such partnerships are likely the institutions with the least financial capacity to accomplish this.

The coming era of institutional consolidation will favor those institutions that are looking forward in coldly realistic ways. Increased endowments will not provide the difference between success and failure for most institutions. Growing net tuition revenue is the key, and this can only be accomplished through effective enrollment growth combined with sensible expense decisions. And for most institutions, this will mean finding ways to increase scale through some form of partnership or consolidation. The alternatives are grim.

Dr. Chet Haskell serves as Co-Head for the College Partnerships and Alliances for the Edu Alliance Group. Chet is a higher education leader with extensive experience in academic administration, institutional strategy, and governance. He recently completed six and a half years as Vice Chancellor for Academic Affairs and University Provost at Antioch University, where he played a central role in creating the Coalition for the Common Good with Otterbein University.

Earlier in his career, he spent 13 years at Harvard University in senior academic positions, including Executive Director of the Center for International Affairs and Associate Dean of the Kennedy School of Government. He later served as Dean of the College at Simmons College and as President of both the Monterey Institute of International Studies and Cogswell Polytechnical College, successfully guiding both institutions through mergers.

An experienced consultant, Dr. Haskell has advised universities and ministries of education in the United States, Latin America, Europe, and the Middle East on issues of finance, strategy, and accreditation. His teaching and research have focused on leadership and nonprofit governance, with a particular emphasis on helping smaller institutions adapt to financial and structural challenges.

He earned DPA and MPA degrees from the University of Southern California, an MA from the University of Virginia, and an AB cum laude from Harvard University.